The Federal Reserve Open Market Committee voted to hold the Fed Funds rate range at 4.25% to 4.50%!

3 Things to Know:

- Today, the FOMC decided to keep the Fed Funds rate range unchanged at 4.25% to 4.50%. This is the second decision in a row in which the Fed Funds rate cuts have been paused.

- In the statement, the Committee inserted the following: “Uncertainty around the economic outlook has increased”.

- The futures market is forecasting approximately 50 basis points of rate cuts by the end of 2025. Specifically, it expects a 25-basis point cut at the July 30th meeting, followed by another 25-basis point cut at the December 10th meeting.

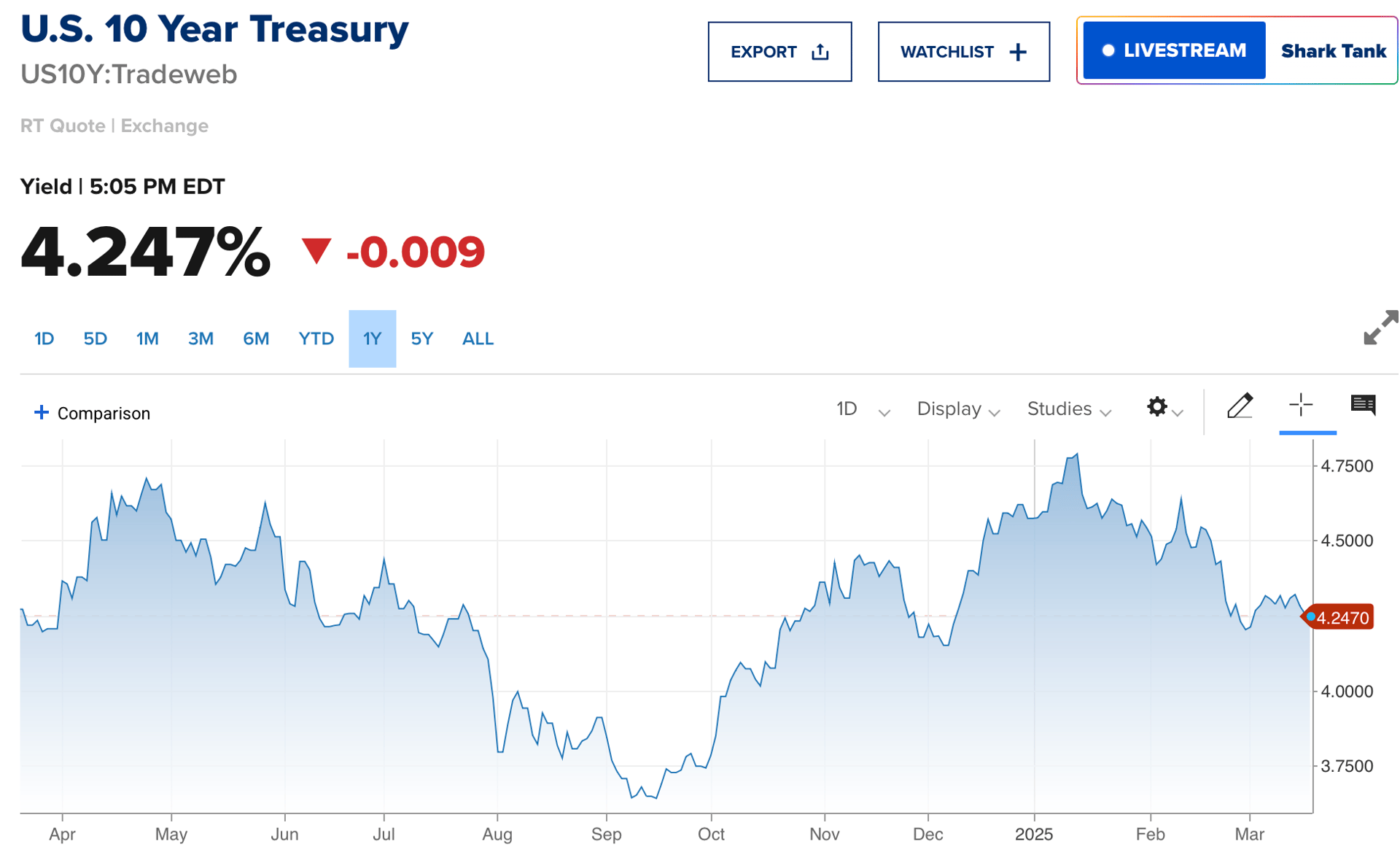

The futures market had almost fully priced in a 100% likelihood that the Fed would keep rates unchanged at today’s meeting, and the Committee followed through with that expectation, opting to pause rate cuts once again. Chairman Powell emphasized that the Committee’s focus is on distinguishing “the signal from the noise.” Here, “signal” refers to reliable economic data, while “noise” pertains to the fluctuating headlines surrounding policy changes. Powell also addressed the current administration’s focus on key areas such as trade, immigration, fiscal policy, and regulation. He noted that the cumulative impact of these policies will shape both the economy and the trajectory of monetary policy. Ultimately, Powell stated that there is no rush to adjust the policy stance and that the Fed is in a strong position to wait for more clarity before making any changes.

What’s Ahead:

In summary, Chairman Powell's outlook is cautious, and his approach appears to be one of patience, emphasizing the need to wait for more clarity. Powell highlighted the ongoing uncertainty in the economy, particularly stemming from the policy changes being implemented by the new administration. The economy is expected to grow at a slower pace than previously anticipated, with GDP growth projections for 2025 revised down to 1.7% according to their latest forecasts. Inflation is expected to rise slightly to 2.7%, with tariffs being highlighted as a key concern. Powell reiterated that the Fed will remain flexible in response to evolving conditions…as always!

Post-meeting, the futures market continues to price in two 25 basis point rate cuts in 2025.

Expectations of major events are typically priced into markets prices before they occur. But sometimes these events are not fully thought through.

How This Hits Real Estate

Interest rates are like the heartbeat of real estate because they mess with mortgage rates. If the Fed does cut rates later, borrowing money to buy a house gets cheaper. That could get more people excited to jump into the housing market, maybe even push home prices up if there aren’t enough houses to go around. Sounds great, right? Well, not so fast. They also said inflation might climb higher, and economic growth could slow down. Higher inflation means stuff like lumber and labor for building homes gets pricier, which could slow down new construction and keep the supply tight. On the flip side, if the economy takes a dip, people might get nervous about their jobs and hold off on buying, which could cool off demand. It’s like a seesaw—cheaper mortgages pulling one way, economic worries pulling the other.

- For Buyers: If you’re looking to buy, now might be a smart time to lock in a mortgage rate. Rates are steady for now, but who knows what’s coming down the road. Getting ahead of any shifts could save you some cash. Also is good moment for negotiations.

- For Sellers: If you’re selling, pay attention to what’s happening locally. Price your place right—too high, and buyers might sit it out if they’re feeling jittery about the economy; too low, and you might miss out if demand picks up from lower rates.

- For Investors: If you’re playing the long game, maybe look at stuff like rental properties in solid neighborhoods. Those tend to hold up better if the economy gets shaky, keeping that cash flow steady.

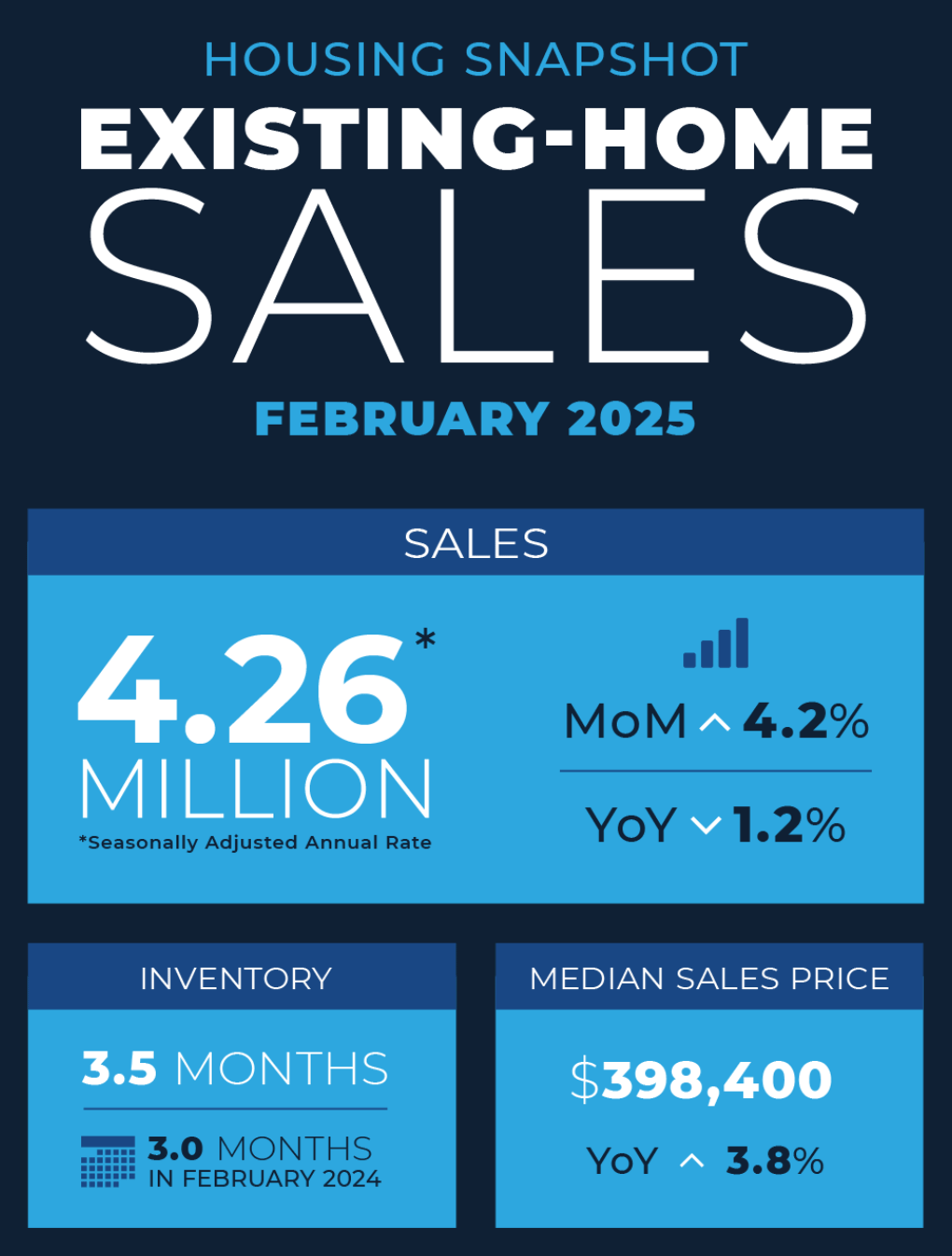

Todays News, U.S. existing-home sales rose 4.2% in February, beating expectations.Some buyers and sellers who’ve been waiting for prices to drop are biting the bullet, according to economists. The median existing-home sales price rose 3.8% from February 2024 to $398,400, marking the 20th consecutive month of year-over-year price increases.

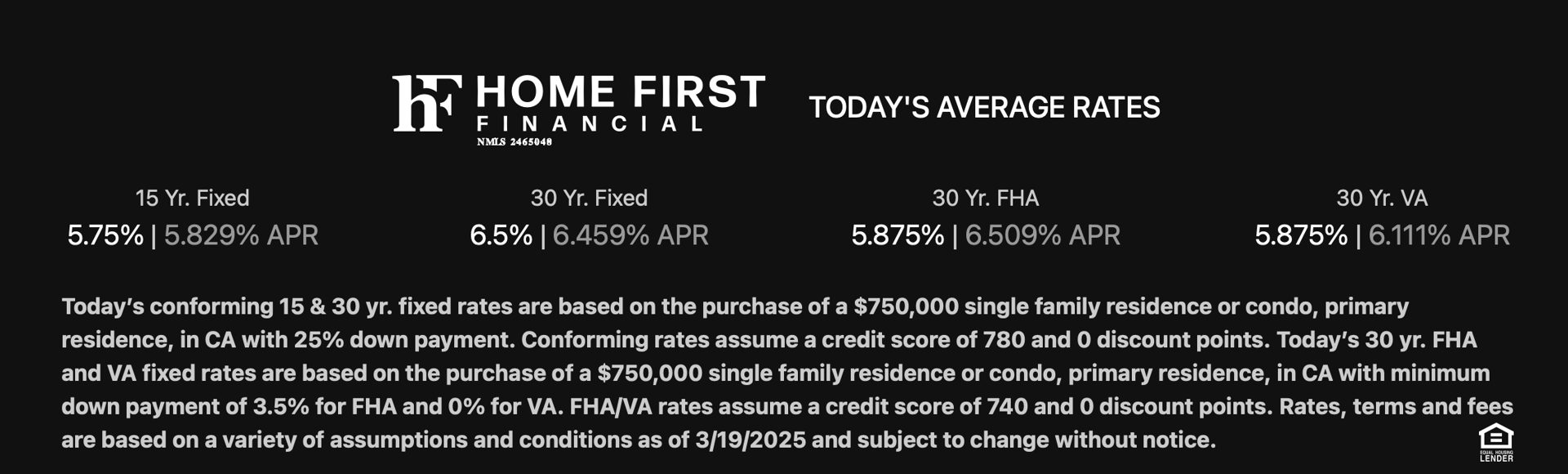

Check with our preferred lenders on rates, there are good programs and remember that the rates change everyday.

The Fed’s playing it cool for now—holding rates steady but leaving the door open for cuts later. For real estate, it’s a bit of a mixed bag: lower rates could spark some action, but economic uncertainty might keep things in check. My advice? Keep your ear to the ground and be ready to pivot. That’s how we’ll stay ahead of this, at Rippe Group we always keep you informed.